I’m on the phone to a friend, a recent mother, talking about children’s nurseries. Specifically, we’re talking about the recent trend for nurseries across London to be snapped up by a breed of investors known as “private equity” — hard-charging capitalists known for ruthlessly maximising businesses in underperforming industries and selling the assets at a massive profit.

“I personally would never send my kid to a private equity nursery, just out of principle,” she says. Childcare is “outrageously expensive” in this country, she explains, and in London particularly, meaning that many women can’t make work pay. “I really don’t agree with private equity effectively exploiting that situation, that ends up fucking loads of women,” she tells me.

The twist? Far from a critic of private equity, this woman has built a very successful career in the sector. In fact, she’s a big advocate of this much-criticised corner of finance: she and her colleagues would argue that they benefit workers, customers and the British economy when they buy up companies and run them better.

“I love our industry and I think we are really good at making businesses more efficient,” she reminds me near the end of our call. “I just don’t think those methods about maximising everything within a business should be applied to looking after my child.” She points me to an Economist article, which notes that child care eats up a much higher proportion of household income in the UK compared to countries like France, and many times higher than Germany.

I don’t have children. And I should declare that until a few weeks ago, I knew very little about the scandalous price of London’s nurseries. But I’m in my mid-thirties, and I’ve detected this topic creeping up the agenda in group chats. I see friends going through the stages of shock, anger and denial as major chunks of their income disappear into the bank accounts of companies with names like Little Muffins and Little Forest Folk.

Here’s an interaction between two friends, both recent parents, in a WhatsApp group over Christmas.

Friend 1: Our local all day nurseries are now £27,500 a year. Not even a fancy one, just a standard chain.

Friend 2: Private equity are such cunts.

Friend 1: £77k salary needed to just cover that bill.

As more of my friends weighed in, I began to wonder: What really is going on with London’s nurseries? And how come private equity investors are seeing pound signs when local independent nurseries are running out of money?

To answer these questions, we first need to understand exactly how private equity got its tendrils into the sector. It’s a story of “roll-ups,” big profits for City financiers, free croissants and the birth of the most depressing metric I’ve ever seen in a business document: “revenue per child”.

A nursery blitzkrieg

Let’s start with that once-obscure kind of investment called private equity. After quietly taking over swathes of the corporate sector, private equity has recently moved into nurseries, too.

A private equity firm invests large pots of money that usually comes from pension funds (for example, the UK’s Universities Superannuation Scheme is a big private equity investor). Pension funds once invested in companies through the public stock market, but recently they’ve been investing in companies privately instead. Private equity uses the pension funds’ money to buy a company, run it typically for five years, and then sell it on. On average, they aim to more than double the pension funds’ money over that time period.

One strategy that’s become increasingly popular over the last 10–20 years involves buying lots of smaller businesses in the same industry and combining them to benefit from so-called ‘economies of scale’. Private equity firms use jazzy names for this, like ‘buy and build’ and ‘roll-up’. So while private equity used to be known for buying companies and breaking them up, these newfangled roll-ups are the opposite of that.

The exceptionally well-paid titans of private equity (it was recently reported that investment banks like Goldman Sachs are having to increase their already enormous pay packets to stop top talent from leaving for private equity) have been applying this approach to a wide range of industries. You’ve probably used private equity-owned businesses without knowing it — they’re now big in vets, crematoriums, holiday parks, special educational needs schools and travel agents, to name just a few. The economies of scale are obvious: instead of each vet practice, for example, needing its own bookkeeper or web developer, the private equity firm sets up a head office function that can spread that cost over many practices.

In the last ten years or so, day nurseries have joined this list. Private equity firms generally buy and combine existing nurseries, rather than starting new ones. The sellers may be the nurseries’ individual founders, in which case this is a way for them to cash out. Increasingly, though, one private equity (or PE firm, as they’re known by finance people) may buy a chain from another PE firm.

By definition, PE firm owners have much more financial firepower than the owners of family-run nursery businesses. The same is even more true for not-for-profit nursery providers, such as charities, which don’t have any shareholders to begin with. This means PE firms are gradually taking over the top end of the sector in terms of size. Ten years ago, Nursery World’s top 25 chains by size included four not-for-profits, of which two were in the top five. In the current list, the largest not-for-profit, the Coop, has slipped to number 12.

How does this work in practice?

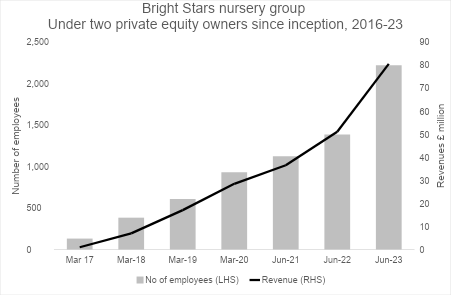

Ever heard of a nursery group called Bright Stars? No? There’s a reason for that. Ten years ago, Bright Stars didn’t exist, but today, depending on whose league table you use, the group currently ranks third or fourth largest in size. It has around 100 nurseries, referred to as “settings”, and an estimated 8,000 children’s places. At least 20 of its nurseries are located across London, including in Hackney, Aldgate, Forest Hill, Hammersmith, Ladbroke Grove, Putney, Wandsworth and Wimbledon.

The explanation why, despite its size, the name Bright Stars may not ring a bell with parents is because the group operates its nurseries under many different brand names. The following logos feature on Bright Stars website for London alone: Northcote House, Elm Park, Zeeba Daycare, Little Muffins, Sunrise and Little Forest Folk.

Sunrise Nursery's virtual tour (Video via Sunrise Nursery on YouTube)

Why so many brands? Because Bright Stars in its current form is the result of two successive private equity owners pursuing aggressive ‘roll-up’ strategies. It all started in 2016, when a newly minted private equity firm called Innervation Capital Partners (ICP) saw an opportunity to buy up individual nurseries or small groups and put them together to form a larger group. This wasn’t a completely new idea, but ICP seems to have gone about it with above-average success.

Starting from scratch, ICP spent the next five years buying a string of nearly 40 existing nursery businesses — roughly one every six weeks, on average. The total cost was around £70 million, of which ICP and its investors put up around £20 million. Many of the companies consisted of a single nursery. ICP put them together into a single group that could benefit from consolidated functions, like finance and HR departments, likely run from the group’s head office in Derby. By June 2021, under its new name Bright Stars, the group had gone from a standing start to around 44 nurseries employing over 1,100 people.

By 2021, ICP had owned this investment for five years, the average holding period for private equity firms. If things are going well — meaning, the private equity firm can make a good profit by selling — they will usually look to pass the parcel. Increasingly, though, one private equity firm may buy a chain from another PE firm. That’s what happened here.

When ICP decided to cash out, the winning bidder was a larger and more established private equity firm called Oakley Capital, whose website says it focuses on “technology, consumer, education and business services”. In June 2021, Oakley paid around £185 million to buy Bright Stars from ICP.

After paying off the loans it had borrowed to help pay for all the nurseries it had bought, ICP said it made a profit of more than £100 million on the Bright Stars investment. It’s unclear how this profit then got split between ICP’s investors and the people who work for ICP itself. There’s no paper trail here: ICP’s website names just four investment professionals. But the sheer size of the figure explains why private equity has overtaken investment banking as the place where people who want to get rich — seriously rich — go to work. And this level of profit also explains why other private equity firms, like Oakley, have become interested in nurseries.

To repeat ICP’s success, Oakley was going to need to keep up the relentless buying spree. In the two years after it bought Bright Stars for £185 million, Oakley spent another £100 million on buying another 20 nursery operators. Within two years, Oakley had almost 2,200 members of staff — almost exactly double the previous number. And turnover had more than doubled too, to £80 million.

This was no organic expansion into the world of childcare. You can get a sense of the breakneck speed of Bright Stars’ expansion by looking at the accounts it had to legally file. After filing its first set of accounts, for the year ending June 2022, the company later had to go back and file three amended sets of accounts in the space of six weeks. Since audited accounts are supposed to be definitive, even one set of amended accounts would be unusual. This might sound like a tedious administrative detail, but it illustrates just how fast this roll-up was taking place and the stresses it was placing on the business.

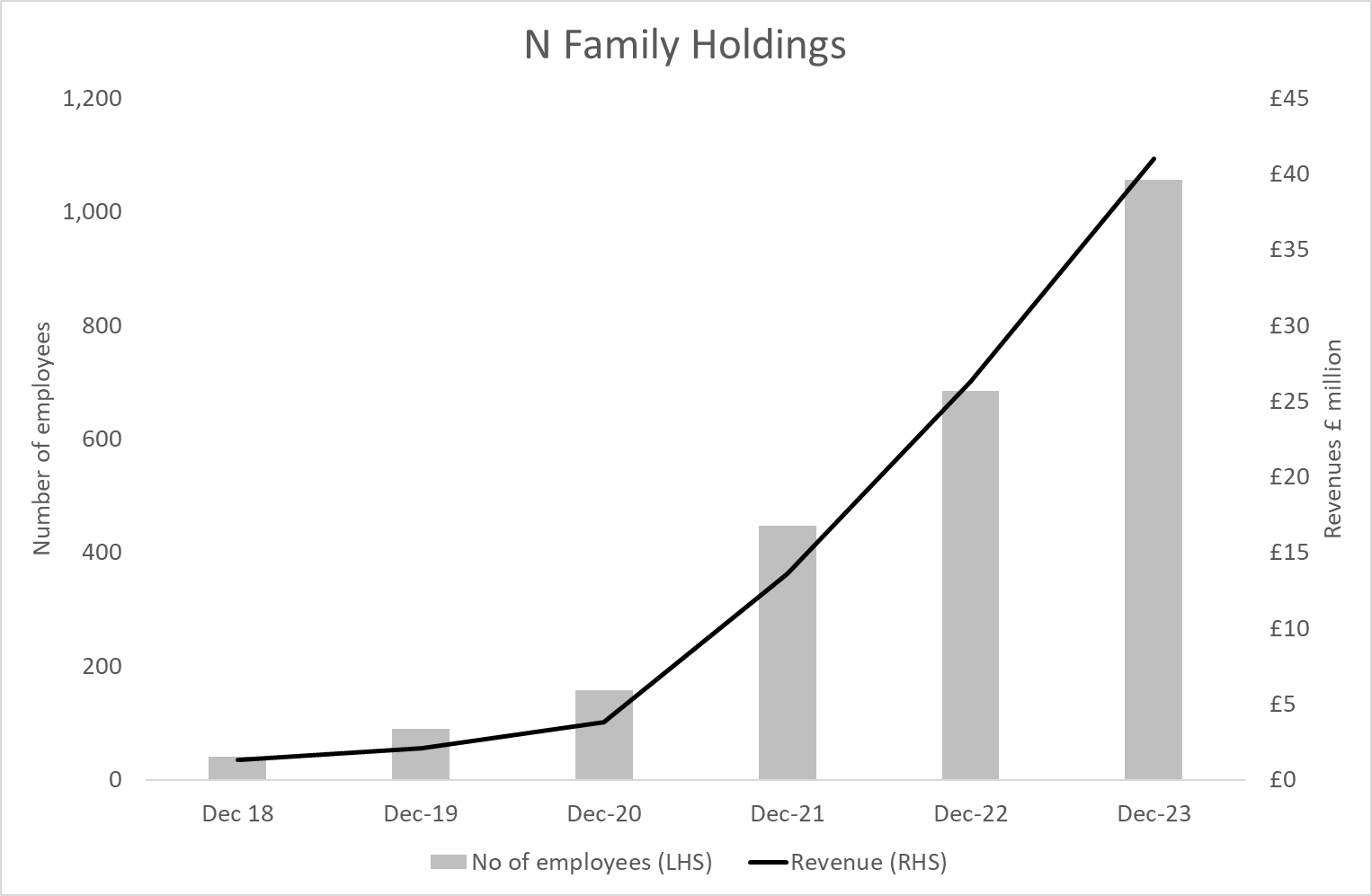

Nurseries run by private equity firms might look like your average local independent. But others are slick, corporate enterprises, their vibes akin to toddler co-working spaces. This is the case for another fast-growing nursery group particularly focused on London: N Family Club. Founded in 2017 by Phil Sunderland, N Family is a high-end offering targeted at professional parents. At drop-off, the website states, they’re “free to grab a coffee and a bagel from the breakfast bar and answer some emails in the parents’ area before heading off to work.”

When I mention N Family to friends, one of them calls it as the “St Paul’s of nurseries”, referring to the ultra-elite, expensive West London private school. Another describes its nurseries as “another level” — meaning free coffees for parents (let’s put “free” in air quotes if you’re paying thousands of pounds a month), music and language classes for the kids and Scandinavian-inspired decor that suggests a luxury Airbnb rather than “a room toddlers are going to throw up in all day”.

Sunderland has retained control of N Family Club by raising money from a range of different investors along the way, including a venture capital firm and the family office of a South African insurance billionaire. The company’s growth rate, which looks similar to Bright Stars, has taken it to around 45 settings, putting it in the top 20 nationally by size. Its website shows more than half (25) of its locations dotted around London, with another 11 in Surrey and Kent commuter land.

Along with its coherent aesthetic, another big difference between N Family and Bright Stars is the way the former uses a single brand. Bright Stars has grown by buying existing nurseries and then retaining the existing brands. N Family’s growth has come mainly from setting up its own nurseries or converting a few existing nursery businesses to its brand. Even though N Family has grown — and continues to grow — incredibly fast, Ofsted nevertheless seem convinced by its quality: in 2023, Nursery World reported that N Family topped the league table when it came to Ofsted ratings for its nurseries.

Who owns your kids’ nursery?

So, if the kids are being well looked after, does it really matter whether your nursery is owned by a private equity firm or not? Well, there’s the issue of transparency. When a private equity firm owns a company, it often becomes somewhere between hard and impossible for outsiders (including customers — in this case, parents) to see basic things like who controls the company; how big it is; and how strong it is in financial terms.

When a company is quoted on the stock market, anyone can go to its website and find an audited annual report. This contains an accurate and comprehensive description of how big the company is, what it owns, and its financial strength. But when it’s a PE-owned nursery group, that isn’t quite so easy. If we look again at Bright Stars, we can see that, after it bought the company in June 2021, Oakley was soon buying again in order to maintain its growth trajectory. In August 2022 Bright Stars paid £4 million to buy out the founders of a group of three companies: Little Forest Folk Ltd, Little Forest Folk Tree Ltd and Little Forest Folk Too Ltd.

There are currently nine nurseries under the Little Folk Forest brand. But, although its website outlines its distinctive approach — “great childcare in the great outdoors” — what it doesn’t seem to mention is who owns these nurseries. There’s no indication that they belong to Bright Stars — the third or fourth-largest nursery group in the country, with a head office in Derby.

Surprisingly, Ofsted doesn’t seem to think this is worth mentioning, either. Take Little Forest Folk Morden, a small nursery with 24 places, which was registered with Ofsted in 2021 and was inspected for the first time in May 2023. At this point, the nursery had belonged to Bright Stars for nearly a year. Ofsted’s inspector rated Little Forest Folk Morden ‘Good’ in every category, but the report provides absolutely no clue as to who ultimately controls this nursery. The ‘registered person’ in the inspection report: Little Forest Folk Ltd.

Little Forest Folk Ltd does still exist: it’s one of the nearly 100 subsidiaries that the Bright Stars parent company lists in its most recent accounts. But if you’re a parent who wants to know who’s ultimately in charge at Little Forest Folk, it’s near impossible to find out. How big is the group it belongs to? Is the group financially sustainable or does it face financial risks? What sort of ratings does the group as a whole get? These are basic questions you’d have thought policy makers, including Ofsted itself, would care about. But instead, they currently leave parents completely in the dark.

Nurseries are not the only sector where the lack of transparency afforded with private equity ownership has been an issue. To take just one example, the Care Quality Commission — which regulates health and social care in the UK — faced fierce criticism for the same reason ten years ago. Southern Cross, the largest care home group in the country, had effectively gone bust thanks to the high financial risk it inherited from previous private equity owners.

In response, parliament now explicitly requires the CQC to pay more attention to the largest care home groups as groups — that is, going beyond the traditional approach of simply rating individual care homes. Where Ofsted is concerned, discussion has begun about how it should rate the performance of academy school chains. But there’s currently no sign of this extending to nurseries.

As the government becomes the dominant customer for nursery services — paying in up to 80% of total sector revenues — shouldn’t it at the very least be requiring more transparency from nursery chains? And why isn’t it preventing a Southern Cross-style collapse by implementing the Joseph Rowntree Foundation’s recommendation and limiting the use of debt? As of March 2024, for example, Bright Stars had borrowed over £180 million to fund its nursery roll-up.

Why does it matter?

But let’s go back to parents for a second, and the crucial question of prices. Even if transparency is important in a policy sense, the majority of parents I’ve consulted for this story —- even ones who are knowledgeable about the workings of private equity — do not seem to care very much about who ultimately owns their kids’ nursery. They pick based on how caring the staff seem to be and, most importantly, whether it seems like the nursery will keep their children safe. And there’s no evidence that corporately owned nurseries have any worse Ofsted ratings than independent ones.

Every year, Nursery World ranks the 25 largest chains in the country based on their nurseries’ Ofsted ratings. N Family Club came top in both 2022 and 2023, before slipping to second place in 2024, while Bright Stars shot up the table in 2024 from thirteenth to sixth. Interestingly, two of the top three spots in 2024 were occupied by a charity that operates only in London (LEYF) and an employee-owned chain called Childbase Partnership (home counties and midlands).

There’s an argument that for-profit nursery operators have more of a stake in trying to bring down metrics like staff turnover, because they know how expensive it is for a business. When one of my friends attended his toddler’s “quarterly review meeting” at a corporate-owned nursery in West London, the staff member looking after their daughter said she much preferred working for this nursery than for her previous employer, a local independent outfit: the staff room was nice, the food was better and the staff got proper breaks.

There’s no reason to think for-profit ownership necessarily gets in the way of good nursery care, any more than there is to think not-for-profit ownership always results in good care. Economies of scale are real, after all: if a standalone nursery can’t spread its payroll costs across a larger chain, it’ll have fewer resources for looking after children. The optimisations that PE companies make to extract their profits from nurseries can be common sense moves, like doing good online marketing so that classes are always full. But when an increasing chunk of nurseries’ income comes from government subsidies, for many people it becomes a point of contention that PE firms are profiting at taxpayers’ expense.

There’s also the pressing question of what might happen in the future as private equity investors increase their grip on local nursery markets. When the primary incentive of the ultimate owners is profit, what does that mean for employees, kids and parents? And what happens if a group goes bust due to its high financial debt? “I think my concern on PE-funded nurseries is that they drive up prices and drive down quality over time. They’re in it to make money,” one of my friends, a mum of two in Walthamstow, tells me. “And is that what you want as the motivating factor for your child’s nursery?”

She admits that’s a somewhat simplistic analysis, but it’s one basically supported by the friend and mother working in private equity who I quoted at the top of this piece, who mentions the dreaded term “dynamic pricing”. “It’s okay if you have normal market forces keeping a lid on prices,” she says. “But with these roll-ups of these local businesses, you can create monopolies in local areas.”

A promotional video for Little Forest Folk (Video via Little Forest Folk on YouTube)

A standard private equity move would be to implement a dynamic pricing model, using the data it has about local demand and supply. In an area where there are only two nurseries, both oversubscribed, the PE-backed company will push up prices. Local independents probably aren’t going to do that as proactively as they don’t have the same access to data, and because the people running the nurseries actually meet parents at the gate every morning.

After a change like the recent rise in National Insurance for employers, don’t be surprised if you see the private equity-owned nurseries passing that cost straight on to parents. These investors aren't sentimental animals — remember, “revenue per child” is paramount.

You shouldn’t be surprised, then, if more London nurseries start installing fancy coffee machines and rolling out slick apps for parents. Another sector of the city’s economy is being gobbled up and rationalised by the kings of private equity. Quite apart from any practical consequences, for some people, this just doesn’t sit right.

Thanks for reading today's article — please do share it with your friends. If you're not already a paid member of The Londoner — entitling you to all of our members-only content — then click the buttons below for a time-limited subscriber discount.

Comments

How to comment:

If you are already a member,

click here to sign in

and leave a comment.

If you aren't a member,

sign up here

to be able to leave a comment.

To add your photo, click here to create a profile on Gravatar.